StartEngine Newsletter: The Case for a 50/30/20 Portfolio with Pre-IPO Private Equity

May 19, 2025 • 6 Min Read

StartEngine Newsletter: The Case for a 50/30/20 Portfolio with Pre-IPO Private Equity

Dear StartEngine Investors,

Ray Dalio’s principle of “radical transparency” compels us to confront market realities with clarity.¹ The 60/40 portfolio — 60% equities, 40% fixed income — has been a mainstay for its simplicity and balance.²

But markets have shifted, and clinging to old models risks missing new opportunities.

For our accredited investors, I propose a 50/30/20 portfolio†:

- 50% equities – public stocks (broad market exposure)

- 30% fixed income – bonds (to provide balance and income)

- 20% alternative assets

- 10% pre-IPO investing (early-stage private equity opportunities before companies go public)

- 10% in other alternative investments (private credit, real estate, oil and gas, gold, etc.)

This evolution, championed by BlackRock’s Larry Fink and rooted in decades of portfolio research, can offer accredited investors like you a smarter way to diversify.³

Drawing on foundational economic theories, let’s explore why pre-IPO private equity could be a good fit for your portfolio, and how to adopt this model which aims to enhance returns and reduce risk.

The following content is intended only for accredited investors and is for informational purposes. It does not constitute an offer, solicitation, or recommendation to invest in any securities. Private investments are speculative, illiquid, and involve a high degree of risk, including the potential loss of your entire investment. Past performance is not indicative of future results.

†For information about StartEngine’s services, duties, and conflicts of interest, please review our Form CRS and Reg BI disclosure.

Invest in Some of Today’s Most Dynamic Pre-IPO Companies

Don't forget — StartEngine Private allows accredited investors to gain exposure to pre-IPO companies like OpenAI, Perplexity, and Databricks for as low as $15,000.*

The Limits of the 60/40 Portfolio

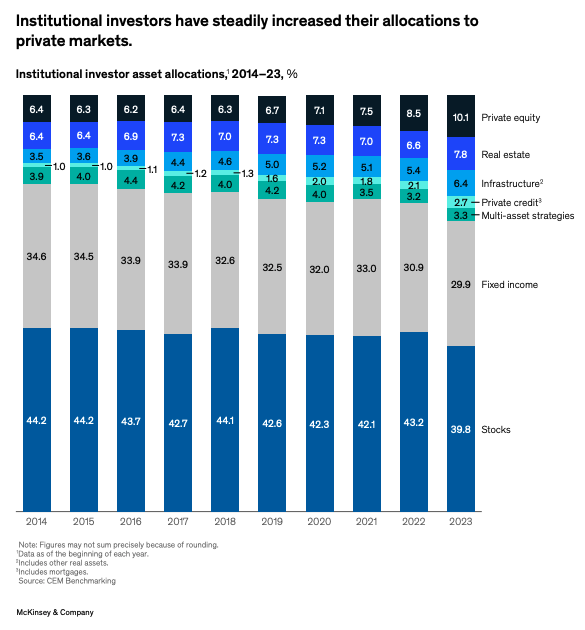

The 60/40 portfolio was born from Modern Portfolio Theory (MPT), introduced by Harry Markowitz in 1952. Markowitz showed that combining assets with low correlations minimizes risk for a given return, plotting optimal portfolios on the “efficient frontier.”²

For decades, stocks and bonds, with correlations often below 0.3, delivered strong results. From 1980 to 2000, the S&P 500 returned about 12% annually, and 10-year Treasuries yielded 6–8%, with relatively low volatility.⁴

But today’s markets challenge this classic model. Public equities have become more concentrated:

- In 2024, the S&P 500’s top 10 firms drove 31% of its value, amplifying systemic risk.⁵

- 10-year Treasuries yielded 4.7% in Q1 2025, but inflation near 3% erodes real returns.⁶

- The 60/40 portfolio’s volatility spiked to 12% annually from 2010 to 2023, per McKinsey, with returns lagging historical norms.⁷

Eugene Fama and Kenneth French, whose 1992 factor models expanded MPT, noted that market inefficiencies persist in concentrated markets, reducing diversification benefits.⁸

Source: McKinsey. Institutional allocations may differ from individual-investor needs; historical shifts do not guarantee future results

Why Pre-IPO Private Equity? The Economic Case

Enter pre-IPO private equity: investments in high-growth startups before they go public.

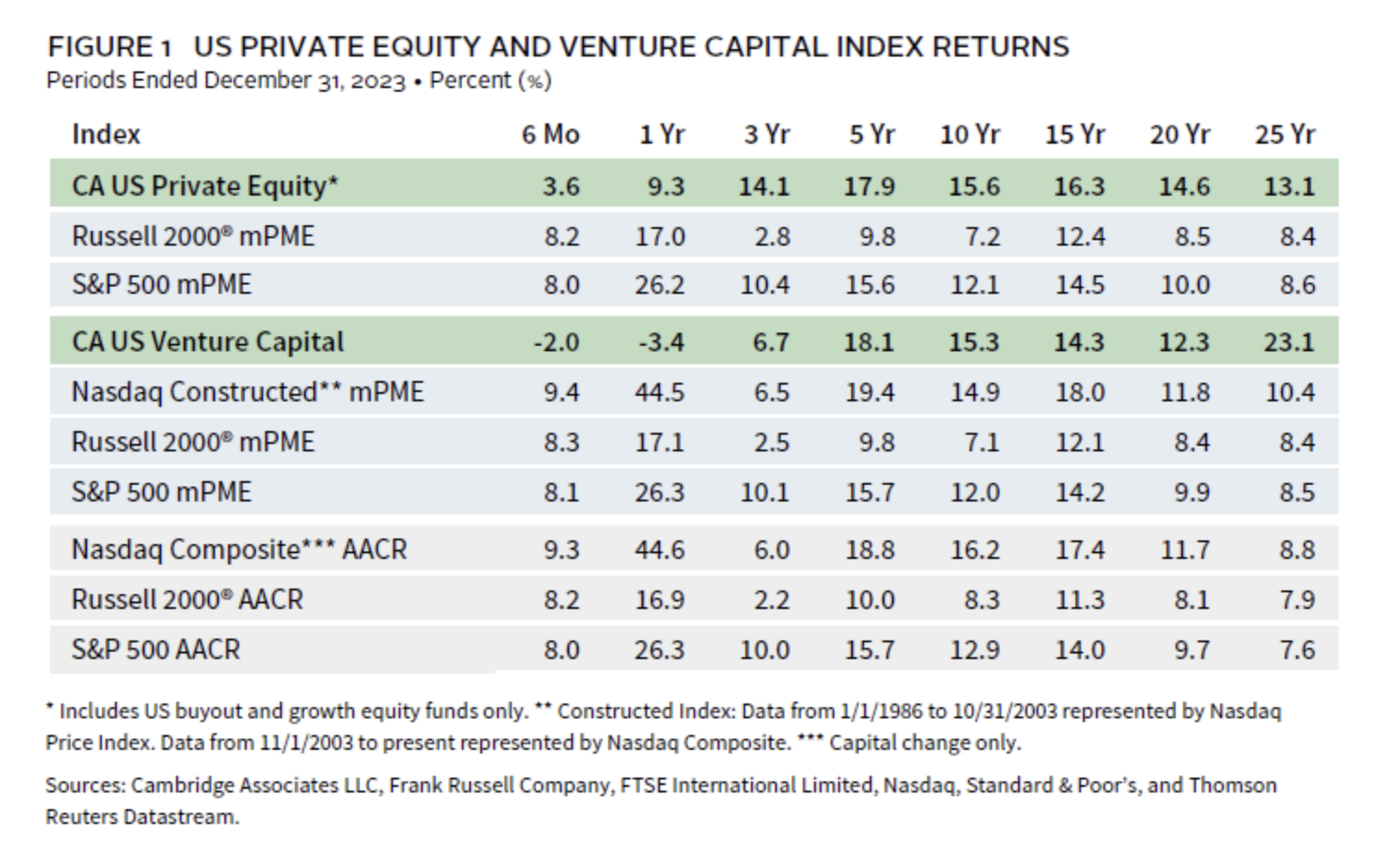

These assets, with correlations of 0.4 to equities and 0.1 to bonds, align with MPT’s diversification logic. Cambridge Associates data shows private equity averaged 13.1% annualized returns from 2000 to 2023, outpacing the S&P 500’s 7.5%.⁹

This example is extraordinary and may not be representative of typical investment outcomes in private markets, and investors should be aware that past successful results are not indicative of future performance.

Economists like Robert Merton, who extended MPT with intertemporal models, argue for including alternative assets to capture long-term growth. Private equity’s illiquidity — capital locked for 5–10 years — suits patient investors, as Merton’s 1971 work on horizon-based investing suggests.¹¹

During the 2008 crisis, private equity fell 20% less than public equities, recovering faster, per Bain & Company. In 2022’s bear market, venture-backed firms showed valuation resilience, insulated from public market panic.¹²

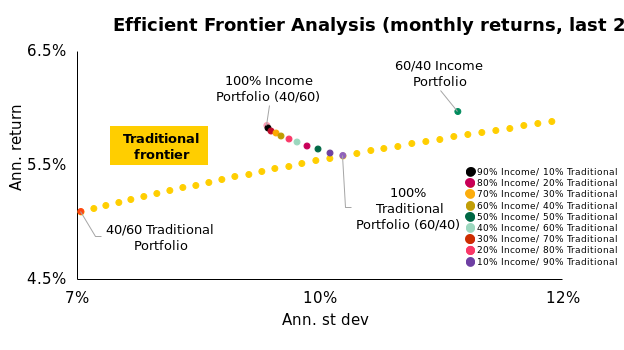

The 50/30/20 model leverages these insights. William Sharpe, creator of the Sharpe ratio, emphasized risk-adjusted returns. Private equity’s Sharpe ratio was 0.9 from 2010 to 2023, versus 0.6 for public equities, per McKinsey.⁷

By allocating 20% to pre-IPO, you shift the efficient frontier upward, achieving higher returns (7.2% vs. 6% for 60/40) with lower volatility (9.8% vs. 12%), as BlackRock’s 2025 analysis confirms.³

While historical data suggests private markets have outperformed public equivalents over certain periods, past performance is not indicative of future results. Future returns may vary significantly and are subject to multiple factors, including economic conditions, market trends, and individual investment risks.

Source: BlackRock. Private-equity and other alternative assets introduce illiquidity and the potential total loss; diversification cannot guarantee gains or prevent losses.

Portfolio Theory’s Evolution to 50/30/20

This model isn’t a hunch — it’s data-driven. The 50/30/20 model builds on decades of research:

- Markowitz’s MPT laid the foundation.²

- Fama and French’s 1992 three-factor model highlighted how small-cap and value stocks — analogous to pre-IPO firms — drive outsized returns.⁸

- Merton’s 1990 continuous-time models showed illiquid assets suit long-horizon investors.¹¹

- Dalio’s 2005 “all-weather” portfolio, balancing risk across asset classes, inspired Fink’s push for private markets.¹

Bain’s 2024 report notes private equity now manages $14 trillion, rivaling public sectors, as IPOs dropped from 400 in 2000 to 150 in 2024.¹²

The 50/30/20 allocation is intended to balance risk parity, as Sharpe’s 1994 CAPM extensions suggest, reducing the risk that a single asset dominates volatility.

Why Should You Consider Private Equity?

You’re accredited — earning over $200,000 annually or with a net worth above $1 million — so you have legal access to pre‑IPO investments.¹³ That access can expand your opportunities, but diversification is still key.

A 10% allocation to pre-IPO, diversified across 10–20 investments, may broaden growth exposure while helping to diversify overall portfolio risk. While the familiar 60/40 mix has merits, its heavy reliance on concentrated public equities and inflation-sensitive bonds can increase volatility. A 50/30/20 framework, informed by the work of Markowitz, Merton, and Sharpe, aims to improve these risk-adjusted returns and add access to earlier-stage innovation (though outcomes may vary and private investments can result in total loss of capital).

Consider the data: From 2000 to 2023, private-equity funds delivered an annualized 13.1 % net return, compared with ~7.5 % for the S&P 500, according to Cambridge Associates.⁹ McKinsey estimates that adding a 20 % private-equity sleeve to a 60/40 portfolio would have lowered overall volatility by about 18 % over the same period.⁷ In today’s markets—where IPO counts are falling and public-equity benchmarks have grown more concentrated—a measured pre-IPO allocation may offer additional diversification.

Source: Cambridge Associates

Building and Managing Your 50/30/20 Portfolio

Here’s is a potential path toward making the transition:

- Equities (50%): consider broadly diversified, low-cost index funds or ETFs like Vanguard’s VTI or BlackRock’s iShares MSCI World. Keeping total expenses below roughly 0.10 % can help preserve net returns. Review and rebalance the equity sleeve at least annually to maintain target weights.

- Fixed Income (30%): consider bond ETFs like iShares AGG or short-duration Treasuries which may help offset equity volatility. Shorter maturities typically reduce interest‑rate sensitivity but also lower yield, so select duration in line with your liquidity horizon and risk tolerance.

- Alternative Assets (20%):

- Private Equity (10%): Allocate to diversified late-stage or pre-IPO investments, targeting 10–20 companies. Invest gradually (5% per year over four years) to avoid vintage risk. Offering documents disclose placement mark‑ups and carried‑interest terms (often ~20 % of net profits).

- Other Alternatives (10%): consider exposure to areas such as real-estate, private credit, oil and gas and other commodities to add further diversification. Evaluate each opportunity’s fee structure, liquidity constraints, and tax treatment before investing.

- Management: Monitor public markets monthly and rebalance as needed; understand that pre-IPO or private holdings are long‑term and may not have short term liquidity. Expect updates on liquidity events (IPOs, acquisitions). Consult a fiduciary advisor to align with your goals.

Invest in Some of Today’s Most Dynamic Pre-IPO Companies

You shouldn't need a Silicon Valley address to get into venture-backed deals. StartEngine Private provides accredited investors with exposure to pre-IPO companies like OpenAI, Perplexity, and Databricks.* The difference? Our investment minimums can be as low as $15,000 —not the seven-figure minimums often required to buy into venture-backed deals.

Risks and Realism

Dalio’s transparency demands honesty: pre-IPO investing carries significant risks. Upfront fees and profit shares raise costs. Illiquidity locks capital, and valuations can be opaque. The SEC restricts pre-IPO to accredited investors for a reason. Visit www.investor.gov and consult an advisor.

The Path Forward

The 50/30/20 portfolio, rooted in the work of Markowitz, Merton, Fama, Sharpe, and Dalio, could be your blueprint for today’s markets. A diversified approach to Pre-IPO private equity can be a calculated move to capture growth and reduce risk. The 60/40 model served us well, but progress demands change. Adopting 50/30/20 could help you build a resilient, high-return portfolio.

Let’s invest smarter, together.

Best,

Howard Marks

CEO, StartEngine

Important Disclosures

This article may contain forward‑looking statements and projections. These are not guarantees; actual outcomes may differ materially.

Investing in private, pre‑IPO companies is highly speculative and illiquid. Such investments are intended only for accredited investors who can bear the risk of total loss. Past performance does not guarantee future results. Consult a financial advisor before investing.

Securities offered through StartEngine Primary, LLC, member FINRA/SIPC. This is a general investment recommendation for accredited investors under Regulation Best Interest; it is not personalized investment advice. Review our Form CRS and Reg BI disclosure to understand our services and conflicts.

*StartEngine Private: The underlying companies held by StartEngine Private Funds LLC, and StartEngine Private LLC (together, “StartEngine Private”) are not participating or involved in the offering. The availability of company information does not indicate that the company has endorsed, supports or otherwise participates with StartEngine Private or any of its affiliates. StartEngine Crowdfunding LLC purchases shares from current and former employees, early investors, and advisors of the companies and sells the shares to StartEngine Private for each offering. When you make an investment in a company on StartEngine Private, you are purchasing an interest in a series of StartEngine Private Funds LLC or StartEngine Private LLC, each a Delaware limited liability company (together the “Series LLCs”), which were created to hold shares of privately held companies. An investor will not directly own or hold shares of the private company but instead will own member interests in a series of the Series LLCs, which either directly or indirectly, will hold shares in the company. There may not be a one-to-one economic parity on the value of the Series LLCs interests and the underlying shares.

Sources:

1. Source: Ray Dalio, “Trust in Radical Truth and Radical Transparency,” Blog, Accessed May 1, 2025

2. Source: Morgan Stanley, “The Future of the 60/40 Portfolio,” Blog, August 13, 2024

3. Source: Larry Fink, “2025 Annual Chairman’s Letter to Investors,” BlackRock, April 2025

4. Source: Macrotrends, “S&P 500 Historical Annual Returns,” Accessed May 2, 2025

5. Source: Greg Iacurci, “Is the U.S. Stock Market Too ‘Concentrated’? Here’s What To Know,” CNBC, July 1, 2024

6. Source: Sean Conlon & Sawdah Bhaimiya, “Treasury Yields Fluctuate After Data Shows Economic Contraction and Greater Inflation,” CNBC, April 30, 2025

7. Source: Fredrik Dahlqvist, et al., “Global Private Markets Report 2024: Private Markets in a Slower Era,” McKinsey, March 28, 2024

8. Source: Beverly Goodman, “Back to School: Fama, French Discuss Their Work,” Barron’s, January 4, 2014

9. Source: Caryn Slotsky, Drew Carneal, Wyatt Yasinski, “US PE/VC Benchmark Commentary: Calendar Year 2023,” Cambridge Associates, August 2024

10. Source: Jeannine Mancini, “How Early Airbnb Investors Raked In A 499,900% Return On IPO Day From A Simple Idea To Pay The Rent,” Yahoo! Finance, May 12, 2023

11. Source: Savina Rizova, “Celebrating Groundbreaking Research with Giants of Finance: Robert C. Merton,” Dimensional Fund Advisors, June 21, 2023

12. Source: Hugh MacArthur, et al., “Private Equity Outlook 2024: The Liquidity Imperative,” Bain & Company, March 11, 2024

13. Source: The U.S. Securities and Exchange Commission, “Accredited Investors,” Accessed February 14, 2025

Get private market investing insights straight to your inbox

Free. No spam. Unsubscribe any time.

Stay up to date on startup investing — subscribe to the StartEngine newsletter

Free. No spam. Unsubscribe any time.

Get the latest Equity Crowdfunding & StartEngine news straight to your inbox

Get the latest Equity Crowdfunding & StartEngine news straight to your inbox

Related Articles

Get the latest Equity Crowdfunding & StartEngine news straight to your inbox

Get the latest Equity Crowdfunding & StartEngine news straight to your inbox