Equity Compensation: What It Means for Employees

December 24, 2025 • 8 Min Read

Equity Compensation: What It Means for Employees

Key Takeaways

- Equity compensation generally refers to ownership-based incentives offered by a company to employees as part of their total compensation package.

- It may include stock options, restricted stock units (RSUs), employee stock purchase plans (ESPPs), or other equity-linked instruments that provide potential ownership stakes.

- Such compensation potentially aligns employee and company interests but involves financial considerations, tax implications, and valuation uncertainties.

Equity compensation generally refers to non-cash compensation that provides employees with an ownership interest in the company or the right to acquire such an interest in the future. Rather than receiving only salary and traditional benefits, employees may be granted stock options, restricted stock units, or similar instruments that tie a portion of their compensation to company performance.

Companies may offer equity compensation to attract and retain talent, particularly when cash resources are limited or when aligning employee incentives with long-term business outcomes is a priority.

Equity compensation is not a guaranteed to provide economic benefit. In many cases, the value depends on future events such as vesting milestones, increases in share price, or liquidity opportunities like a public offering or acquisition.

Common Types of Equity Compensation

Each type of equity compensation involves different mechanics, tax considerations, and potential financial outcomes. The structure chosen by a company may depend on factors such as company stage, regulatory environment, and compensation strategy.

How Equity Compensation Works

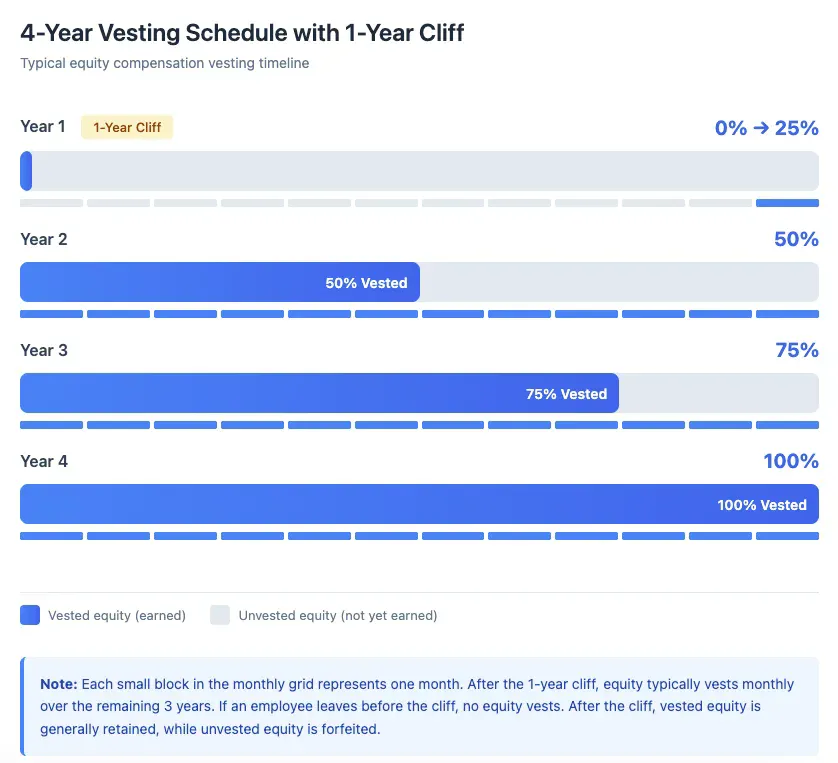

Vesting Schedules: Vesting generally refers to the process by which an employee earns the right to equity over time. Vesting schedules may be time-based, requiring employees to remain with the company for a specified period, or performance-based, contingent on achieving certain business milestones. A common time-based structure involves a four-year vesting period with a one-year cliff, meaning no equity vests until the employee completes one year of service, after which vesting occurs gradually.

- Exercise Price: For stock options, the exercise price (or strike price) is the fixed amount an employee pays to purchase shares. The potential value of the option depends on the difference between the exercise price and the fair market value of the shares at the time of exercise. If the market value exceeds the exercise price, the option may have intrinsic value; if not, the option may be considered "underwater" and may not provide financial benefit upon exercise.

- Liquidity Events: Liquidity generally refers to the ability to convert equity holdings into cash. In private companies, liquidity opportunities may be limited until a qualifying event such as an initial public offering (IPO), acquisition, or secondary market transaction occurs. Public company employees typically have more immediate access to liquidity through established stock exchanges, though blackout periods and trading restrictions may apply.

Potential Benefits for Employees

- Financial Upside Potential: If the company's valuation increases over time, the value of equity holdings may appreciate accordingly. Employees who hold stock options or RSUs may realize financial gains if they are able to sell shares at a price higher than their cost basis.

- Alignment of Interests: Equity compensation may create a shared interest between employees and other stakeholders in the company's success. This alignment could potentially influence employee motivation and engagement, as personal financial outcomes become linked to business performance.

Potential Risks for Employees

- Valuation Uncertainty: The value of equity is not guaranteed and may fluctuate based on company performance, market conditions, investor sentiment, and broader economic factors. In private companies, determining fair market value may involve subjective appraisals and periodic 409A valuations, which may change over time. Share prices in public companies may be volatile, and past performance does not indicate future results.

- Liquidity Constraints: Employees of private companies may face significant liquidity challenges, as there may be no established market for selling shares. Even after equity vests, employees might need to wait for a liquidity event to realize value. Public company employees generally have more options for selling shares, but lock-up periods, trading windows, and insider trading restrictions may limit timing and flexibility.

- Tax Implications: Equity compensation may trigger tax obligations at multiple stages, including grant, vesting, exercise, and sale. The specific tax treatment depends on factors such as the type of equity, holding periods, and applicable tax regulations. For example, ISOs may receive favorable tax treatment under certain conditions, while NSOs typically result in ordinary income recognition upon exercise. RSUs generally result in taxable income upon vesting.

- Forfeiture Risk: Unvested equity is generally forfeited if an employee leaves the company before the vesting schedule is complete. Additionally, some equity agreements may include expiration dates, requiring employees to exercise options within a certain timeframe after departure or risk losing them entirely.

Equity Compensation in Startups vs. Public Companies

- Startups and Private Companies: Startups may rely heavily on equity compensation to attract talent while conserving cash resources. Early-stage equity grants may offer higher potential upside if the company grows substantially, but they also involve greater uncertainty regarding valuation and liquidity. Employees may need to wait years for a liquidity event, and there is no guarantee that such an event will occur or result in favorable financial outcomes. Private company equity may also be subject to transfer restrictions and right of first refusal provisions.

- Public Companies: Public companies typically offer equity compensation within the context of established stock markets, providing more predictable valuation and liquidity opportunities. RSUs are commonly used, and employees may be able to sell vested shares on public exchanges, subject to company policies and regulatory requirements. The potential upside may be more moderate compared to early-stage startups, but the risks associated with illiquidity and valuation uncertainty are generally reduced.

- Company Maturity and Equity Structure: As companies mature, their equity compensation programs may evolve. Early employees may receive larger equity grants with higher risk and reward potential, while later employees may receive smaller grants with more defined value. The choice between stock options, RSUs, and other instruments often reflects company stage, cash availability, and compensation philosophy.

What Employees May Want to Consider

- Review Grant Documents Thoroughly: Equity agreements typically include important details such as vesting schedules, exercise prices, expiration dates, and conditions under which equity may be forfeited. Understanding these terms may help employees make informed decisions about timing and strategy.

- Understand Tax Treatment: The tax implications of equity compensation can be complex and may vary based on the type of equity, holding periods, and individual circumstances. Consulting with qualified tax professionals before exercising options or selling shares may help employees plan for potential tax liabilities and optimize their approach.

- Maintain Clear Documentation: Keeping organized records of grant agreements, vesting schedules, exercise transactions, and cost basis information may be important for tax reporting and financial planning purposes.

- Consider Personal Financial Goals: Equity compensation is one component of overall financial planning. Employees may want to evaluate how equity holdings fit within their broader financial objectives, risk tolerance, and liquidity needs.

Conclusion

Equity compensation generally represents a form of ownership-based pay that may align employee interests with company performance and long-term success. While such compensation potentially offers financial upside if company valuation increases, it also involves complexities related to vesting, taxation, liquidity, and market risk.

Employees considering or holding equity compensation may benefit from understanding the specific terms of their grants, the tax implications at various stages, and how equity fits within their overall financial planning. Consulting with qualified financial, tax, and legal professionals may provide valuable guidance tailored to individual circumstances.

Frequently Asked Questions (FAQ)

Q1: When do employees usually receive value from equity?

Employees typically receive value when shares vest and are either sold or exercised during a liquidity event such as an acquisition, initial public offering, or secondary market transaction. The timing and amount of value realized depend on company performance, market conditions, and the specific terms of the equity grant.

Q2: Can employees lose their equity if they leave the company?

Yes, unvested equity is generally forfeited upon departure from the company. Vested stock options may have a limited exercise window after termination, often 90 days, after which they may expire. Some agreements may allow partial vesting or extended exercise periods under specific conditions such as retirement or disability, but terms vary by company and grant agreement.

Q3: Should employees expect guaranteed returns from equity compensation?

No. The value of equity compensation depends on company performance, market conditions, and timing of liquidity events. Share prices may increase, decrease, or remain flat, and there is no assurance that equity will ever provide financial gain. Employees should evaluate equity compensation as a potentially valuable but uncertain component of total pay.

Disclaimer: This article is for informational purposes only and does not constitute legal, tax, investment, or financial advice. Equity compensation involves complex financial and tax considerations that vary based on individual circumstances and applicable regulations. Employees should consult qualified professionals before making decisions related to equity compensation, including exercising options, selling shares, or evaluating tax implications. Past company performance does not indicate future results, and the value of equity may fluctuate or be lost entirely.

References:

Get private market investing insights straight to your inbox

Free. No spam. Unsubscribe any time.

Stay up to date on startup investing — subscribe to the StartEngine newsletter

Free. No spam. Unsubscribe any time.

Get the latest Equity Crowdfunding & StartEngine news straight to your inbox

Get the latest Equity Crowdfunding & StartEngine news straight to your inbox

Related Articles

Get the latest Equity Crowdfunding & StartEngine news straight to your inbox

Get the latest Equity Crowdfunding & StartEngine news straight to your inbox